22 / 258

22 / 258

[

] 20

those whose wealth derives from cash crops, while these

better-off family farms are differentiated from resource-

poor households that are employed locally. In the middle

are the food self-sufficient with a median level of productive

resource endowments, relying partly on part-time non-farm

activities.

10

In the Malian cotton zone, better-off family

farms possess two or more animal traction equipment units

and 10 or more cattle, while those with less than one animal

traction equipment unit and/or who only use manual labour

are the poorest, and those in between have one animal trac-

tion equipment unit and less than 10 cattle.

In Southern and Eastern Africa farm typologies are largely

based on the discrepancies in landholdings, alongside market

orientation. On average, small-scale family farms hold less

than 3 hectares of arable land and/or cropped areas; middle-

scale capitalist farms hold an average 10-200 hectares, and

LSCFs and plantations hold 500-3,000 hectares.

11

About

20 per cent of small-scale family farms are mainly market-

oriented producers of both food and cash crops, while the

rest are semi-subsistence producers focused on food crops.

Otherwise LSCFs are profit-oriented specialized cash crop

and/or livestock farms, mostly managed as corporate entities.

Contribution of family farms to agriculture

Although most family farms in SSA are largely devoted to

production for auto-consumption, they sell a limited but

significant amount of staple food crops and cash crops

harvested from relatively small areas. In general, family farm

production strategies are shaped by their diverse dietary

requirements, which are often structured around mass energy

staples, pulses and vegetables, with frugal supplies of animal

protein. Thus, family farms tend to allocate some (if not most)

of the family land and labour to producing their main staple

foods rather than cash crops, although a small proportion

of them specialize in the latter. However, when the volume

of produce from all family farms is aggregated, their output

dominates domestic agricultural production in SSA, despite

the higher financial value of the cash crops produced mainly

by LSCFs and better-off family farms.

The bulk of SSA cropped areas is worked by family farms, and

this area has increased by 85 per cent. The cropped area consti-

tuted 43 per cent of arable land area in 1961 and 50 per cent in

2012, showing that a larger proportion of arable land is used

for cropping. In per capita terms the rate of the cropped area

declined slightly considering the low level of inputs utilized on

the continent. Cropped area per capita decreased slightly from

0.24 ha/person in 1961 to 0.11 ha/person in 2012, whereas

arable land per capita declined sharply from 0.54 ha/person

in 1961 to 0.22 ha/person in 2013, which is approximately

1.3 hectares per family. This trend is striking because a higher

proportion of arable land is being cropped per capita, and the

available arable land is close to full utilization.

The scope of production and productivity among family

farms in SSA is differentiated according to their varied social,

agroecological and economic conditions, largely in relation

to their uneven extent and varied forms of integration into

different kinds of commodity and inputs markets. Their social

differentiation is reflected in the changing scale of their land-

holdings, cropped areas and livestock, the rise of wage labour

relations, greater shifts in the purpose of production towards

market, and their increased consumption of varied foods and

other consumer goods fromwithin the family farm and beyond.

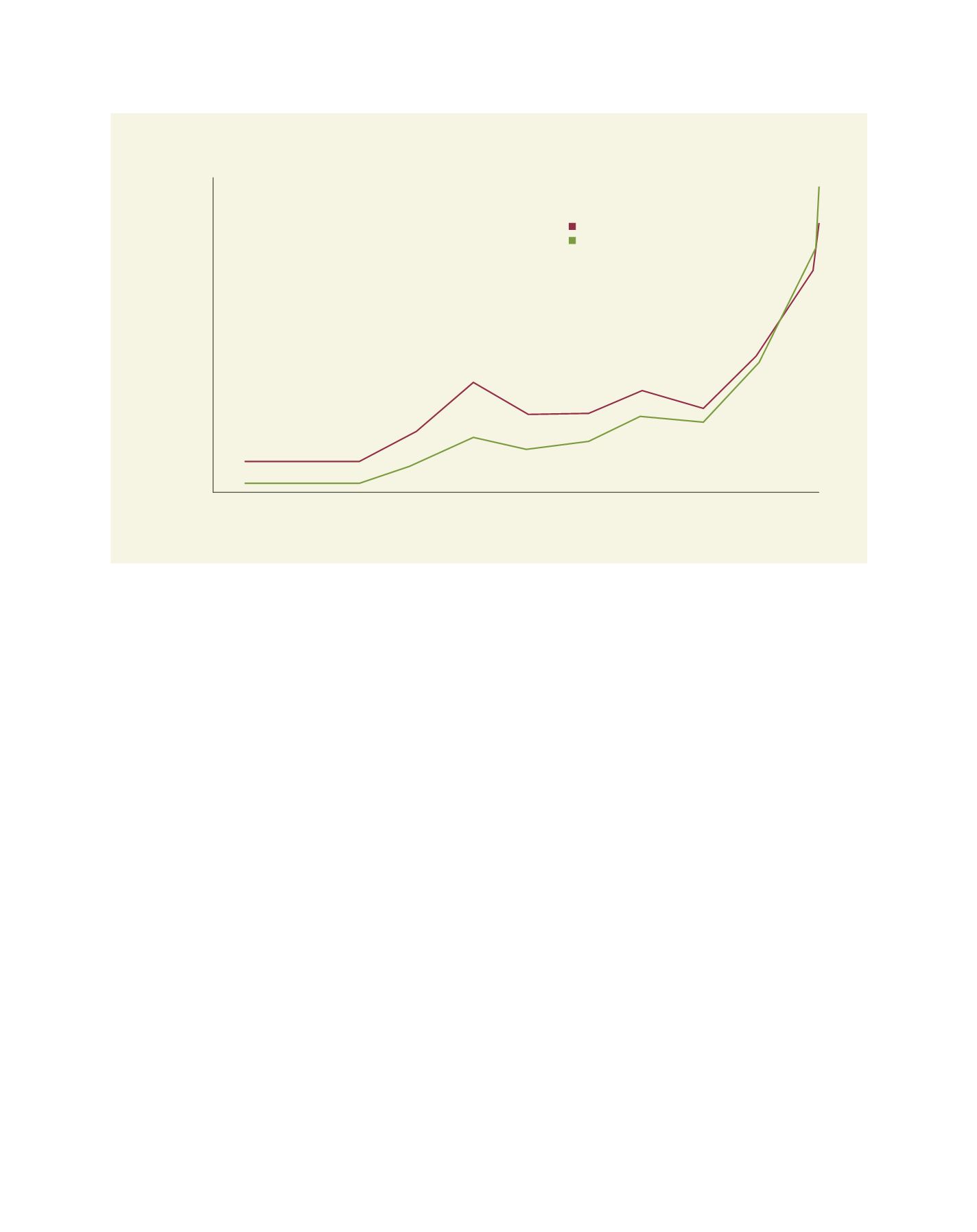

SSA agricultural imports in value and per capita

Source: FAO STAT 2014

1960

0

5,000,000

10,000,000

15,000,000

20,000,000

25,000,000

30,000,000

35,000,000

40,000,000

45,000,000

Import value (1,000 US$)

Imports p.c. (US$/person)

1970

1980

1990

2000

2010

Import value

Import value per capita

R

egional

P

erspectives