64 / 196

64 / 196

[

] 62

New forms of private-public risk transfer:

making societies more resilient

Reto Schnarwiler, Head, Business Development Governments, Swiss Re

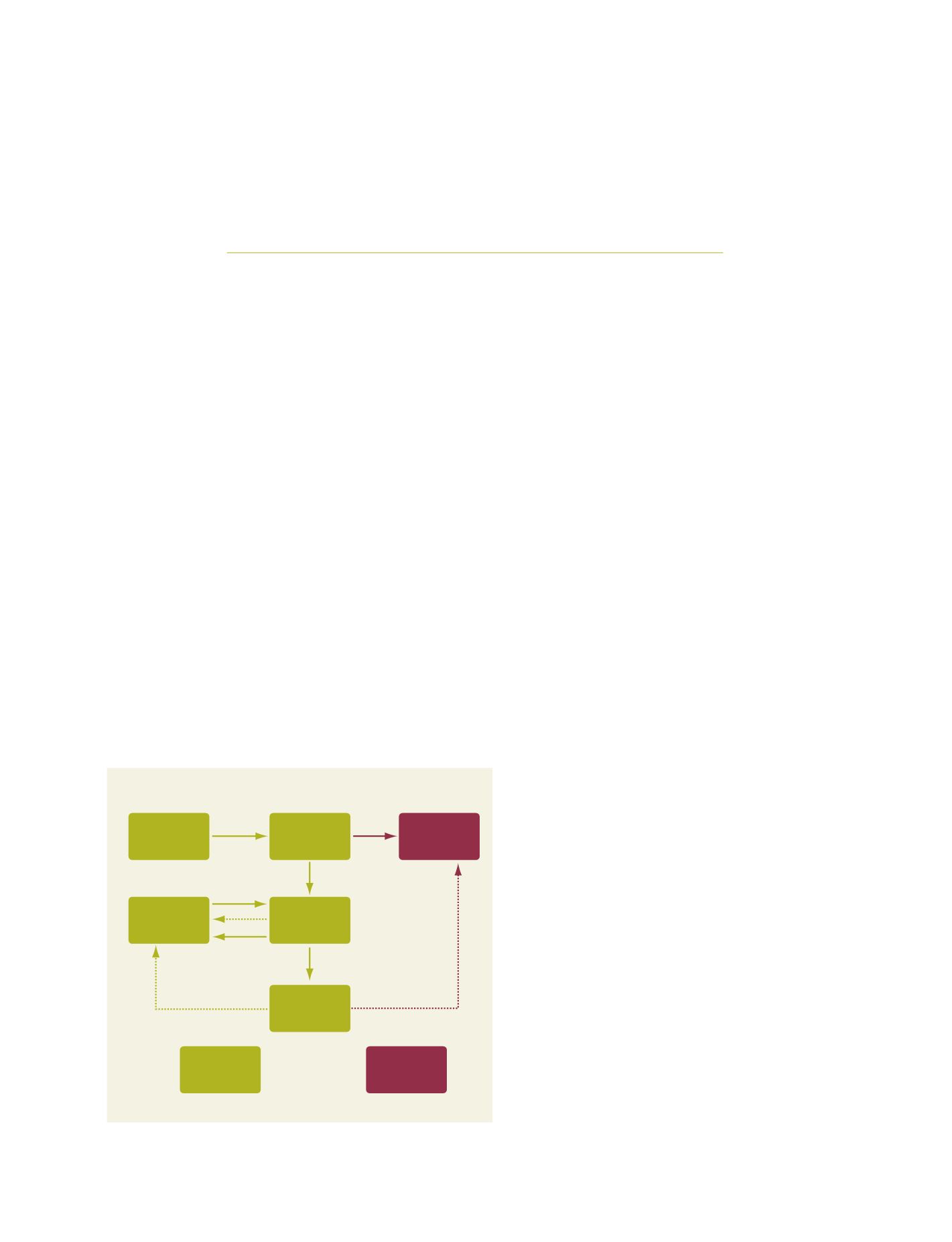

Taxpayers/

donors

Government/

charity

Government/

charity

Investors

GlobeCat Ltd

Trust

Public funds/

donations

Proceeds

Interest

Notes

Proceeds

(SPV)

Principal

repayment

at maturity

Principal

paid as

disaster funds

No catastrophe

event

Catastrophe

event

How the GlobeCat platform works

Source: Swiss Re

T

he rising impact of natural catastrophes is driving up the

cost of disaster relief and reconstruction for the public

sector. New forms of private-public partnership can make

societies more resilient by absorbing the financial impact of large

catastrophes. Such partnerships allow governments, semi-

governmental agencies, aid organizations and non-governmental

organizations (NGOs) to manage disaster expenses more effi-

ciently by funding them before – instead of after – a catastrophe

occurs. One recent example of this approach is the GlobeCat

securitization structured by Swiss Re.

GlobeCat: a new transaction model

In December 2007, Swiss Re used new financial instruments to trans-

fer Central American earthquake risks to the capital markets, using a

very innovative trigger mechanism. The GlobeCat securitization

provides a payout based on the size of population exposed to a speci-

fied earthquake. The transaction provides a newmodel for governments

and relief organizations to access pre-event financing, in order to fund

the growing impact of natural disasters in developing countries.

The GlobeCat transaction is an example of how governments and

NGOs can efficiently secure funding through capital market securiti-

zations. It uses an innovative trigger to determine coverage based on

an index of the population exposed to specified levels of

ground-shaking intensity, as measured by the Modified

Mercalli Intensity scale.

Parametric triggers based on independent factors such

as affected population, crop levels, wind speeds or earth-

quake intensity are ideal for public sector entities, which

typically carry broad relief and infrastructure rebuild-

ing expenses that are not linked to a particular damaged

property. As they avoid the need for damage assessment,

such triggers allow for the swift payment of funds. Due

to their independent – and typically scientific – nature,

they are also preferred by investors.

The goal of the GlobeCat transaction is to create a

platform and model by which charitable foundations,

governmental relief organizations and corporations can

leverage donations, government funds or international

aid in order to reduce the burden of future natural disas-

ters. Such a programme will help public sector

organizations become more proactive in planning and

anticipating relief needs in areas of the world affected

by severe catastrophes. If a triggering event happens, the

funds will be quickly available for relief efforts rather

than being raised after the event.

GlobeCat has shown that this concept is viable, and

that the leverage of own funds to coverage can be as high

as 45 times. For example, USD1 million of donations or

government funds can be used to secure contingent

disaster relief funds of USD45 million. Structures such

as GlobeCat provide swift access to relief funding, and

offer a means to increase contingent funding for cata-

strophic events by using public funds and donations to

purchase coverage on the capital markets.

Natural catastrophes: a rising burden for society

The impact of natural catastrophes on societies and

economies has increased considerably over the last two

decades and is likely to grow further as a result of two

complementary trends. Firstly, climate change is

expected to increase the scale and frequency of major

weather-related events. Secondly, the economic severity

of natural catastrophes is growing due to a rise in both

population and economic activity in areas with a high

risk exposure. In addition, the nature of the risk is

changing, for a variety of reasons. Buildings have

become more expensive to build and repair, and higher

interdependencies in the production process have