32 / 156

32 / 156

Hurricane activity in the North Atlantic and climatic setting

Recent scientific findings in climate research confirm that the trop-

ical cyclone hazard in the North Atlantic has increased markedly

since the mid-1990s. Cyclones there have become more intense and

have been reaching very high wind speeds for longer periods of time.

This increase in intensity is associated with a global increase in sea

surface temperatures, averaging approximately 0.5°C (0.9°F) during

the summer season in all tropical ocean regions since 1970. A

comparison of the recorded trend and computer simulations reveals

that this warming can only be the result of anthropogenic climate

change. Globally, the annual number of strong tropical cyclones (cate-

gories 4 and 5 on the Saffir-Simpson Scale) has more than doubled,

from around eight in the early 1970s to 18 in recent years.

In the North Atlantic, it is not only the intensity that is increas-

ing but also the frequency. The primary factor for this is –

according to scientific studies – the natural cycle of sea surface

temperatures (Atlantic multidecadal oscillation or AMO). The

record number of cyclones in the 2005 season coincides with what

current data indicates to be the highest mean annual temperature

measured in the North Atlantic since records began around 1870.

This is most likely due to the simultaneous influence of two

processes that determine sea temperature and hurricane activity:

natural climate oscillation in the Atlantic, and the long-term

warming process caused by anthropogenic climate change.

Building vulnerability

Catastrophe events of recent years have provided the insurance indus-

try with a vast amount of claims data that has also enabled

conclusions to be drawn regarding the effectiveness of mitigation

measures discussed in the aftermath of major historic disasters.

Some key observations were made in the wake of the US hurri-

canes of 2004 and 2005. As seen in the Florida hurricanes of 2004,

newer residential constructions typically fared much better during

Hurricane Katrina than older buildings, due to the relative newness

of their structural components.

However, new buildings in Louisiana and Mississippi did not

perform as well as in Florida, because neither Louisiana or Mississippi

had statewide residential building codes enacted at the time of the

storm. Both states left the adoption and enforcement of building

codes up to local municipalities, and only a few opted to take such

measures. When compared with Florida, which has strict wind design

codes, differences in new buildings’ performance were apparent.

Mitigation measures that are effective in preventing wind damage

to buildings, such as hurricane shutters and seawalls, are practically

nonexistent along the Gulf Coast outside of Florida, except in some

affluent residential neighbourhoods. To protect a building against

wind damage, it is extremely important to keep its envelope intact.

Window shutters are very effective because they resist wind pres-

sure better than glass and they can protect windows from being

shattered by flying debris. This lack of shutters and other protection

measures is likely to have led to increased property damage due to

blown-in windows and subsequent wind and water damage.

Consequences for the insurance industry:

new loss distributions

The loss statistics from natural catastrophes clearly indicate a long-

term trend toward higher costs. Besides socio-economic reasons,

changing weather patterns and only limited mitigation measures are

the key drivers responsible for this adverse development. What is to

be done from a risk-taker’s perspective?

The insurance industry must adjust the assumptions at the very

basis of its definition of hazard (windstorm, flooding) where scien-

tific data and studies provide strong indications that this is

necessary. Science has made considerable progress in this area,

particularly in 2005. For instance, today we know that the descrip-

tion of a hurricane hazard as the average of a time series of over

100 years cannot serve as the basis for adequate risk management.

This discussion has focused on changing hurricane frequen-

cies and vulnerabilities in the US due to the outstanding hurricane

catastrophes of 2004 and 2005 in the context of long-term loss

trends. However, Munich Re is continuing its analyses of natural

climate cycles and the effects of climate change with regard to

hazards in other regions too, such as tropical cyclones in the

Pacific and Indian Ocean and winter storms in Europe. This will

enable us to anticipate future changes in risks and incorporate

them in risk models.

[

] 32

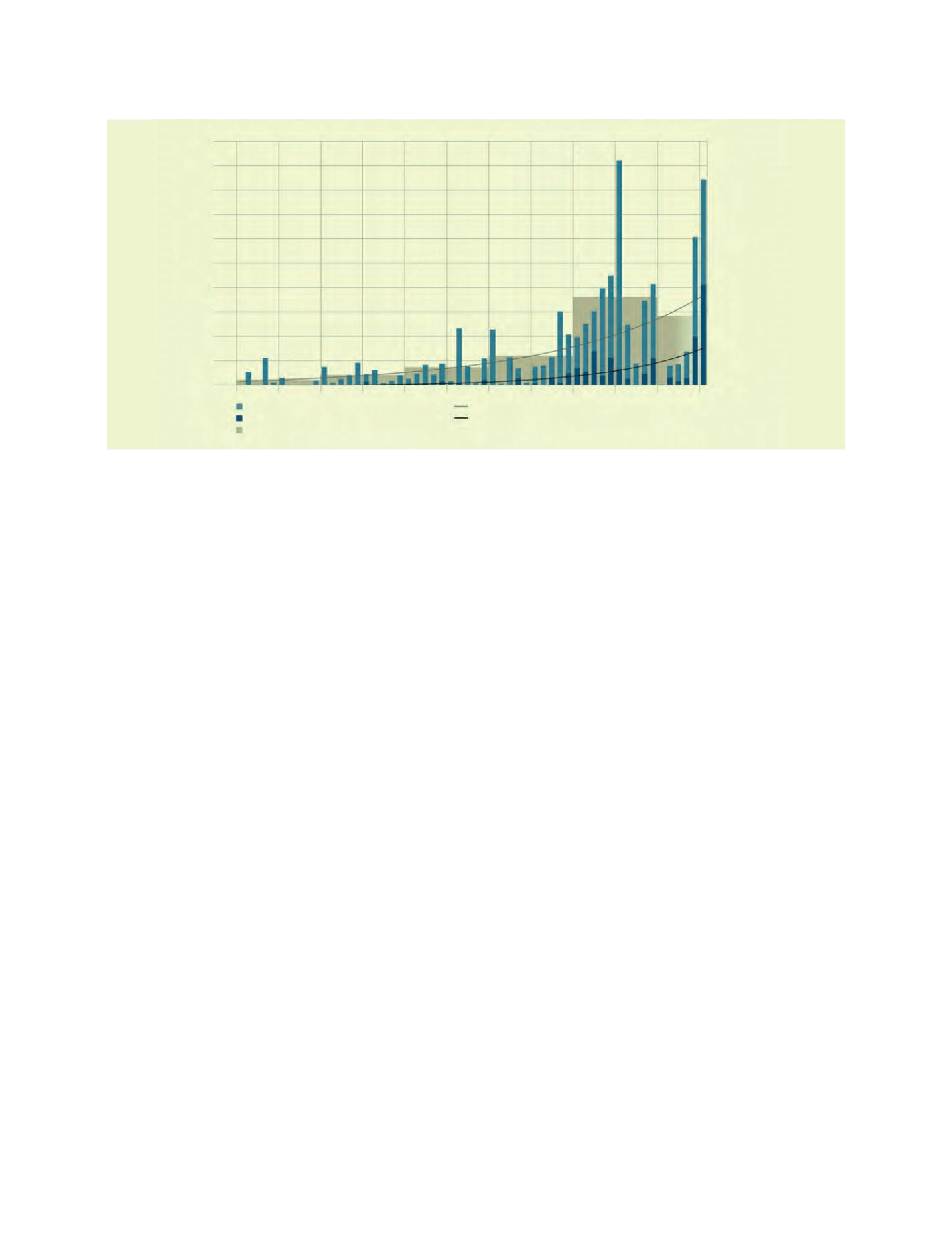

1950

1955

1960

1965

1970

1975

1980

1985

1990

1995 2000

2005

Trend: Insured losses

Trend: Overall losses

Of which insured losses losses (2005 values)

Overall losses (2005 values)

Decade averages of overall losses

0

20

40

60

80

100

120

140

160

180

USD bn

Source: NatCat

SERVICE

, Munich Re

Great natural catastrophes 1950-2005, Overall losses and insured losses – Absolute values and long-term trends