34 / 156

34 / 156

ling companies. Traditionally, modelling companies have based their

forecasts on averages, calculated over a period of 100 years or so. No

explicit account was taken of shorter-term phenomena with decadal

intervals of higher or lower than normal years of storm activity.

In early 2006, one of the leading modelling companies announced

that it was adopting a five-year, forward-looking view of risk for esti-

mating potential catastrophe losses rather than using a long-term

historical average baseline in its modelling. This was done to address

the company’s perception that there is likely to be a period of more

frequent and more intense storms related to higher sea surface

temperatures in the tropical North Atlantic, and to associated

changes in the atmosphere. As a result, the modelling company’s

US hurricane model will increase modelled annualized insurance

losses by 40 per cent on average across the Gulf Coast, Florida and

the Southeast, and by 25-30 per cent in the Mid-Atlantic and

Northeast coastal regions, relative to those levels derived using long-

term 1900-2005 historical average hurricane frequencies.

Ratings agencies have also changed their methodologies as a

result of the severe hurricane season. In the autumn of 2005,

insurance information company A.M. Best announced that it

would continue to use the Best Capital Adequacy Ratio (BCAR),

but will update the underwriting risks to reflect the current envi-

ronment. According to A.M. Best, these changes are not likely to

lead to rating downgrades. However, reinsurers are responding

to the rating and modelling changes by reducing limits in high

catastrophe zones as well as attempting to move exposures to

other financial sectors.

Capital comes charging

The losses of 2005, compounded by the pressure for more capital

from ratings agencies, have led to the need for more risk capital.

Capital markets have responded in a dynamic fashion to this need

for more risk transfer. For example, within a few months following

Hurricane Katrina, the group of 17 top reinsurers in Bermuda had

replaced all of the capital lost in 2005. At the same time, capital was

forthcoming to finance the start-up of 13 new companies.

Further evidence that insurance markets had attracted the inter-

est of investors can be observed in the increased activity in

catastrophe bonds, which directly link investors to insurance risk.

In 2005, total issuance was a record USD2 billion, a 75 per cent

increase over the USD1.14 billion of issuance in 2004. And this

momentum has continued in 2006. In fact, based on our knowl-

edge of transactions completed this year and those in the pipeline,

total new issues in 2006 could be double those of 2005.

1

In terms of less direct investment in reinsurance ventures,

following the record losses from Hurricane Katrina, new capital

raised for insurance and reinsurance entities exceeded USD20

billion, of which USD8.5 billion went to new start-ups.

Hedge funds increased their presence in insurance markets in

2005, investing in start-up reinsurers and other insurance vehi-

cles, or ‘sidecars,’ which were brought to the market after the

2005 hurricanes. A sidecar is a special purpose vehicle in which

third-party private investors, such as hedge funds, provide extra

[

] 34

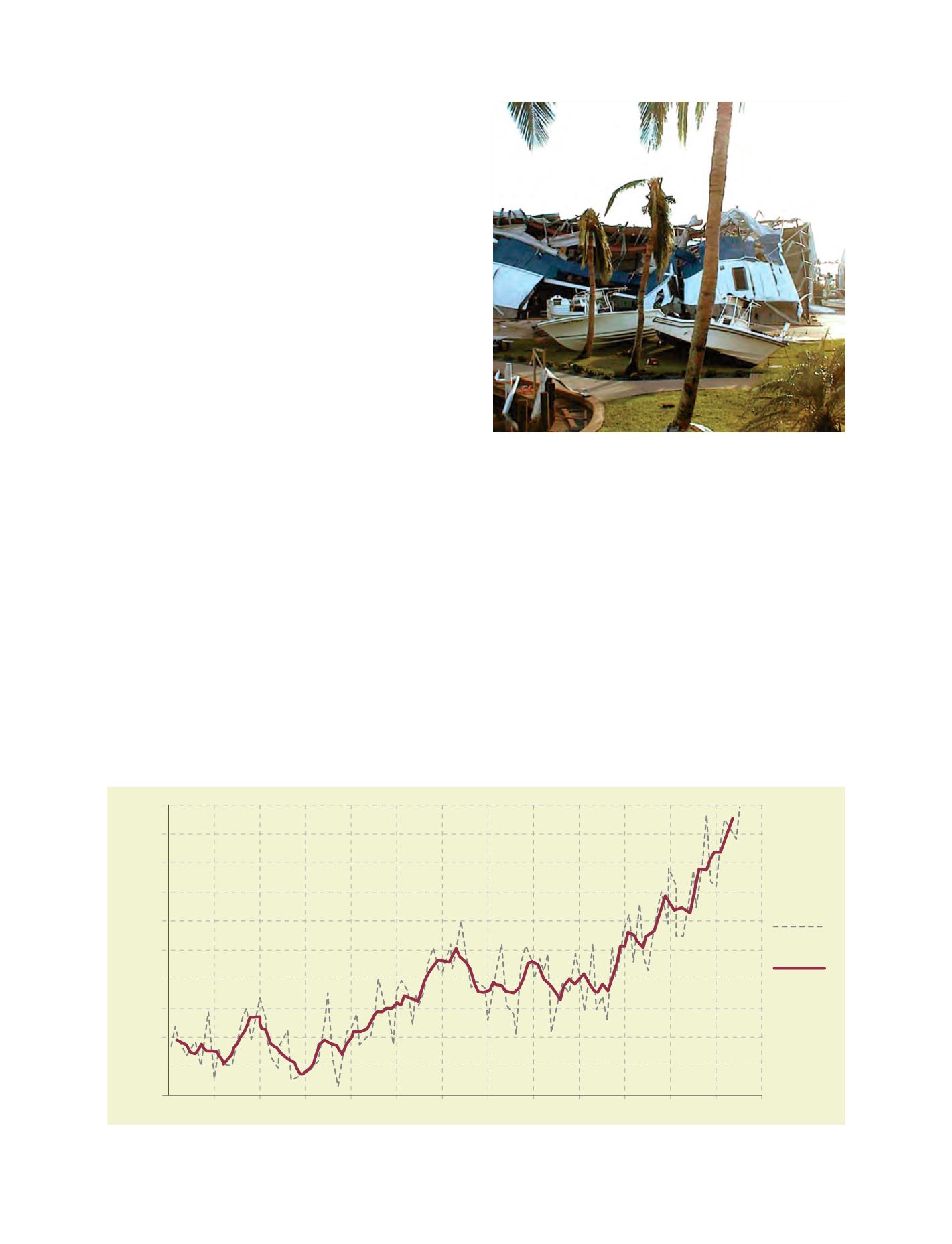

Hurricane damage in the Caribbean

1880

-.4

-.2

.0

.2

.4

.6

1900

1920

1940

1960

1980

2000

Temperature Anomaly (˚C)

Annual Mean

5 Year Mean

Hurricane severity: Increases in land and sea temperature

Source: Goddard Institute for Space Studies, Global Temperature Increases

Photo: courtesy of Herman Kokojan