39 / 156

39 / 156

together under one policy. According to a recent study by the

International Labour Office, 45 per cent of the microinsurance

schemes researched cover only a single risk.

12

Only 16 per cent

of schemes cover three risks, making

Afat Vimo

one of the most

simple and comprehensive products in India. This not only makes

the policy more attractive to clients, but also makes investment

in it more efficient in economic terms. Another aspect that sets

Afat Vimo

apart from other microinsurance policies is the exten-

sive range of eventualities covered. To combine micromitigation

with microinsurance, community capacity building and involve-

ment in

Afat Vimo

has provided more stability and viability.

Reducing an entity’s disaster risk is possible through increasing

that entity’s physical/material, social/organizational, and behav-

ioural/motivational capacities.

13

Using this framework,

Afat Vimo

is successful in reducing community risks to disasters.

Physical/material goods are insured and can be replaced after loss

and damage; social/organizational capacity is supported as informal

businesses are brought together and receive a product unafford-

able to individuals directly; motivational/behavioural capacity is

built as understanding of risk and disaster issues is increased.

International initiatives have strengthened the impact of

Afat

Vimo

. The Hyogo Framework for Action has brought attention,

discussion, resources, and commitment to disaster risk reduc-

tion and to finding opportunities to address it. The United

Nations (UN) Year of Microcredit facilitated commitments via the

‘Disaster risk mitigation: Potential of microfinance for tsunami

recovery’ conference in October 2005. Delegates spoke on the

strengths of microfinance as a tool for poverty and disaster risk

reduction, and experiences of microcredit and tsunami recovery.

The

Afat Vimo

team was able to exchange lessons with other prac-

titioners on its microinsurance product and how microfinance

may be used for recovery. It learned about opportunities working

with primary stakeholders to combine support grants and

microinsurance services, and was able to share progress and

opportunities from the

Afat Vimo

experience.

Corporate sector

Increasingly, partnerships with private commercial sector actors

are being forged for the application of microfinance and risk

reduction. Much can be learned from private sector insurance

providers in terms of risk management; they have a wealth of

experience that can be shared, and this can facilitate the provision

of microinsurance policies for the poor. AIDMI has engaged in a

commercial partnership with the Life Insurance Company of India

to provide life insurance, and the Oriental Insurance Company to

provide non-life insurance cover under the

Afat Vimo

scheme. It

also continues to raise awareness of the opportunities and bene-

fits of insurance provision to the low-income strata of

communities. There is additional scope within microinsurance

to motivate private sector insurance companies to develop and

provide products for low-income individuals as initiatives for their

own corporate social responsibility.

Challenges

Though defrauding is one of the most common challenges for the

microinsurance sector, AIDMI has experienced only one incident

of a false claim. Premium defaulting is another challenge, and the

retrospective collection of payments from clients can be seen as a

threat to the long-term sustainability of the

Afat Vimo

scheme.

At present, AIDMI must absorb all of the operating costs of the

programme, and recovers only the premium total from the benefi-

ciaries. AIDMI must therefore shoulder all the administration costs

and the costs of premium collection, field visits, supervision and

claims assistance. In terms of long-term sustainability, this means

that unless the clients meet the operating costs, the scheme is not

financially self-sustaining. In addition, there are a number of

reasons why beneficiaries do not renew their policies – migration,

inability to pay, and low desire to renew are believed to be factors.

On a broader scale, commitment among donors and interna-

tional organisations should exist for similar risk transfer initiatives

to refine and thrive. AIDMI is a core manager of the Tsunami

Evaluation Coalition’s forthcoming thematic evaluation on “The

Impact of Tsunami Response on Local Capacities”. Under this

initiative, stakeholders in Maldives and Sri Lanka (in April 2006)

have clearly identified the need for risk transfer. This need, however,

is not articulated broadly and remains latent.

The 2005 Community Survey by AIDMI and the Disaster

Emergency Committee identified low levels of risk transfer aware-

ness among communities of India, Sri Lanka and Indonesia.

Organisations across the Asian Region should identify and initi-

ate opportunities for similar experiments for transferring risk

from the poor.

Next steps

There is clearly scope for additional capacity building exercises

designed to impress upon beneficiaries the long-term benefits of

insurance coverage and the importance of continued coverage.

Additionally, greater emphasis on adherence to the correct proce-

dures for making claims to the insurance companies should

[

] 39

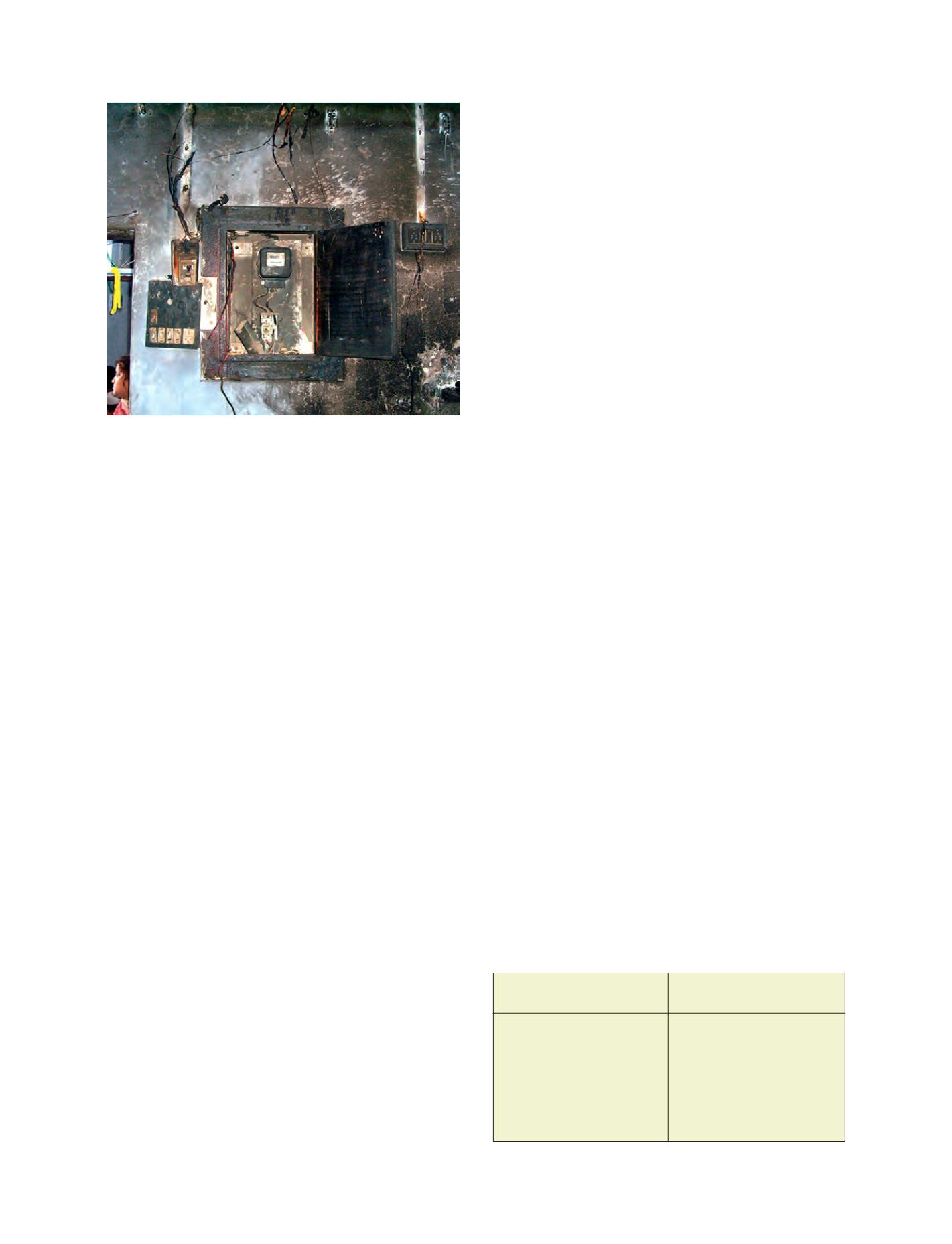

The poor face disasters on a day-to-day basis.

Afat Vimo

covers risks that

have impact on a small and large scale

Photo: AIDMI, Gujarat communal riot recovery 2002

Disasters covered by

Afat Vimo

Cyclone/hurricane, flood,

earthquake, fire, explosion, riot,

malicious damage, aircraft

damage, tempest, inundation,

lightening, implosion, strike,

impact damage, storm, typhoon,

tornado, and landslide.

Typical loss/damage from

disasters in South Asia

Life, income, livelihood assets,

household assets, shelter, health,

livestock, crops.