40 / 156

40 / 156

[

] 40

perhaps be made. This would both reduce the likelihood of claims

being rejected, and increase client satisfaction.

The

Afat Vimo

scheme has tremendous potential for rapid expan-

sion. Currently, microinsurance coverage under the scheme is only

available to communities where AIDMI has presence. Offering a

similar policy in earthquake-affected Jammu and Kashmir and

tsunami-affected areas is being considered. An emergent area of

experimentation and international debate, weather-indexed insur-

ance is being explored as a means of effective management of

catastrophic risk, particularly in vulnerable rural areas. Based on

a round table meeting with the Agriculture Insurance Company of

India and a group of farmers from Kutch, Patan, and

Surendranagar, AIDMI will be covering 1,000 small and marginal

farmers in June 2006 against monsoon. In addition, AIDMI is

about to launch insurance coverage for school children and staff.

Converging interests

In India, partnerships between the commercial sector and NGOs

are increasingly emerging for microinsurance provision. Much

can be learned from private sector insurance providers in terms

of risk management. The impact of

Afat Vimo

has been strength-

ened through national policies that encourage private insurance

companies to provide support to poor clients. The Insurance

Regulatory and Development Authority (IRDA) also plays an

important role in the provision of insurance to the poor. In March

2002, IRDA published a set of regulations applicable to insur-

ance companies operating in India, entitled

Obligations of insurers

to rural social sectors

. Essentially, these regulations establish quotas

of insurance provision to low-income clients.

The establishment of such regulations has greatly increased the

volume of microinsurance policies being supplied to poor clients.

The quota rises each year, reaching a maximum of 16 per cent

after five years of the total number of life policies sold for life

insurance, and five per cent of premium income for other types

of insurance. This condition has generated massive pressure on

insurers, as without selling microinsurance they cannot sell their

more profitable products. IRDA has fined a number of insurers

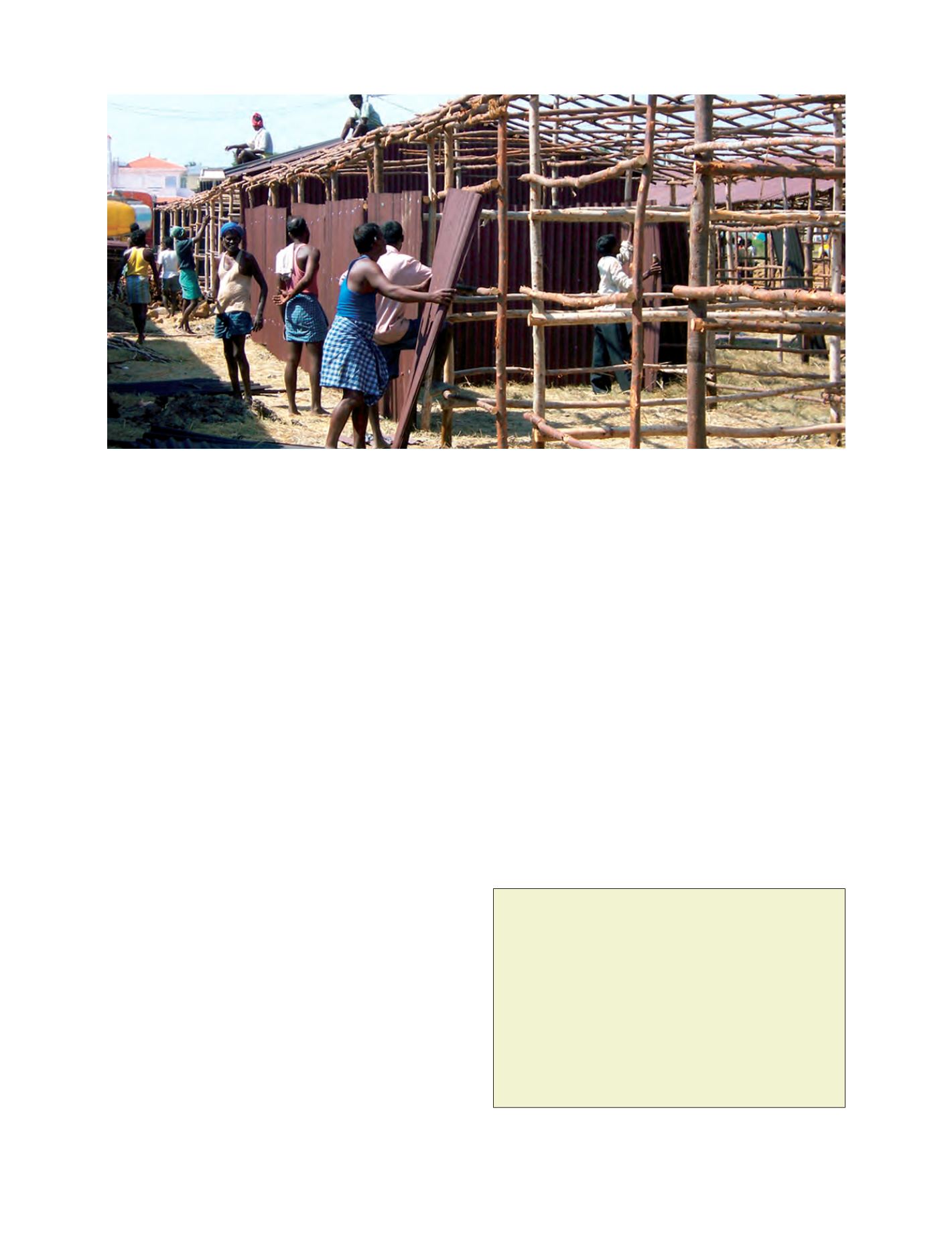

Tsunami recovery is a huge opportunity to transfer financial risks of the poor. Following a major disaster like the 2004 tsunami,

people understand the value of insuring their assets

Photo: AIDMI, Indian Ocean tsunami recovery 2005

Rural areas:

more than 400 population per km

2

or 25 per cent of

workers in agricultural pursuits:

•

Life insurance:

5 per cent of total policies in year 1, up to 16 per

cent in year 5

•

General insurance:

2 per cent of gross premium income in year 1, 3

per cent in year 2 and 5 per cent thereafter.

Social sector:

casual workers, economic vulnerable or backward

classes in urban and rural areas:

• 5,000 policies in year 1; up to 20,000 in year 5 for both life and

general insurance.

Source: Roth, J. et al (2005). ‘Microinsurance and Microfinance: Evidence from India,’

CGAP working group on microinsurance ‘Good and bad practices: Case study #15.’

14

Obligations of insurers to rural social sectors

for failing to meet their targets, but there have also been a number

of perceived and reported problems associated with the imposi-

tion of quotas.

Pro-poor financial risk transfer initiatives combined with risk

reduction measures such as

Afat Vimo

are rare in South Asia.

There is a real potential for disaster risk management at commu-

nity level through insurance. The 2004 tsunami and the 2005

Jammu and Kashmir earthquakes provide a huge opportunity

for local institutions to transfer the future financial risks of

victims by facilitating access to the microfinance services.

However, this is not easy. It needs planning, awareness build-

ing, suitable services, and long-term commitment. Convergence

of interest and attention from academics, researchers, policy

makers, donors, and risk mitigation practitioners along with

victim communities is also highly desirable.

Generating the awareness – and building the commitment –

to initiate microinsurance costs money, time, and effort. These

must be found if

Afat Vimo

is to be suitably resourced. AIDMI

welcomes inputs and ideas for recasting and up-scaling

Afat Vimo

,

or similar microinsurance schemes, in India and outside.