38 / 156

38 / 156

[

] 38

and premiums have been set, AIDMI reconfirms the beneficiaries on

the list and ensures that all the requisite information has been

collated and passed to the insurance companies. Once this is

complete, AIDMI pays the premiums to the insurance companies

on behalf of the beneficiaries, ensuring immediate coverage.

Subsequently, the

Afat Vimo

team begins to collect the premiums

from the beneficiaries. The process is effective but time-consuming

and costly, especially when renewal is optional.

When disaster strikes, the beneficiary immediately informs the

Afat Vimo

team of the occurrence. The team then responds

quickly to process the claim. AIDMI assists beneficiaries in filing

claims properly. Since many

Afat Vimo

beneficiaries are illiterate

or have poor literacy skills, they require this type of assistance.

The need to build this general capability among policyholders is

recognized. Therefore training is provided to help policyholders

understand exactly how they can best use the policy.

Feedback from beneficiaries who have made claims under the

Afat Vimo

policy has been very positive and encouraging. To date,

41 claims have been made, and 23 of these have been success-

fully settled, giving a combined payout of USD5,635. Of the

claims that have been made, ten were for loss of life, 11 for

personal accident (some resulting in fatality, others causing loss

of earnings), two for house fires, and 18 for damage to property

and contents as a result of monsoon flooding.

Success

Microinsurance offers several advantages. It can be a transparent

means of providing compensation against damage, and it

decreases the need for humanitarian aid. Additionally, it offers

those affected by disasters a more dignified means to cope than

relying on the generosity of donors after disaster strikes.

11

Microinsurance may also make tracking trends in vulnerability

and hazards easier when claims are charted with geographic infor-

mation systems.

Part of the success of

Afat Vimo

can be attributed to the afford-

able premium negotiated on behalf of the clients by AIDMI. This

puts insurance within the reach of those who otherwise would

not be able to access conventional insurance services. Similarly,

AIDMI has had a great deal of success in the prompt settlement

of claims, which has translated into client satisfaction and a good

relationship with the insurance companies. It has also contributed

to the good policy renewal rate, which currently stands at 88 per

cent. From an original membership of 829 beneficiaries at the

launch of

Afat Vimo

in August 2004, coverage has grown to a stag-

gering 5,519 members in only 20 months.

Afat Vimo

policyholders

are now spread across several districts in Gujarat, as well as in

Tamil Nadu and Pondicherry in South India.

A particular strength of the

Afat Vimo

scheme is its unified policy

design. Under

Afat Vimo

, life and non-life coverage are brought

While ‘victims’ manage the majority of disaster recovery themselves, microinsurance can help accelerate their efforts

Photo: AIDMI, Jammu and Kashmir earthquake recovery 2005

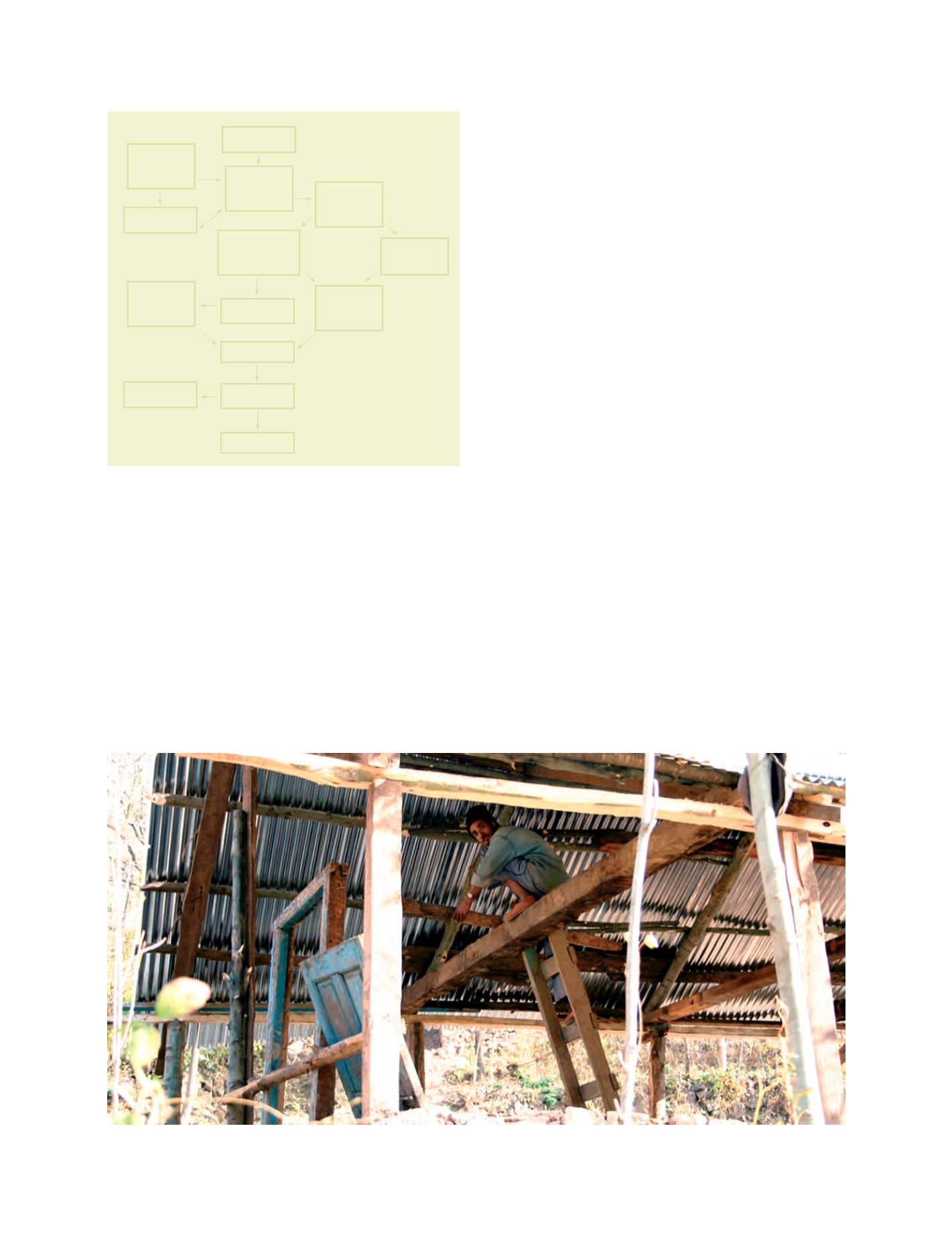

Afat Vimo

Team

explain scheme to

community

Submission of

premiums to

AIDMI accounts

Demand/need

letter from

beneficiary

Complete

Afat Vimo

forms, collect

respective documents

Beneficiary

list submitted

insurer

Premiums

paid by AIDMI

to insurer

Scheme/policy

design

Potential beneficiary

Capacity building

for insurance

Beneficiary

database created

Collect premiums

from beneficiaries

Afat Vimo

member

for one year

Policy handover

Policy renewal

The

Afat Vimo

operating structure

Source: AIDMI