36 / 156

36 / 156

[

] 36

I

N

I

NDIA

,

PERSONAL

, household and small business assets are

often unprotected against disasters. Relief and rehabilitation often

rely on aid to cover the costs, but support from outside entities

is often unpredictable – this makes it difficult to replace the damaged

assets of the poor, thus making recovery difficult. Groups that fail to

recover are more vulnerable to subsequent disasters.

Insurance covers many losses but is often unavailable to the

poor due to the high transaction cost to affordable premium ratio.

Microinsurance has emerged in a policy environment that has

made recent progress towards disaster risk reduction. Recent

insurance regulatory reforms within the Indian Government and

the prioritization of risk reduction by the UN ISDR, the

ProVention Consortium, and DFID have contributed to the viabil-

ity and advancement of microinsurance for the poor.

Afat Vimo

(Gujarati for ‘disaster insurance’) was born in this envi-

ronment as a product of the All India Disaster Mitigation Institute

(AIDMI). Demand for the

Afat Vimo

product has been growing,

and currently covers more than 5,500 small businesses.

Due to a combination of high exposure to natural hazards and

high human vulnerability, South Asia perennially experiences signif-

icant losses to disasters. Present studies estimate that more than 90

per cent of the Indian population does not benefit from any kind

of social protection.

1

Despite high and steady growth in the country,

the cycle of disasters and vulnerability deprives many millions of

poor of the human development that might have accompanied such

growth. Within Asia, 24 per cent of deaths due to disasters occur

in India because of its size, population, and vulnerability.

2

Since

2004 alone, India has faced two major disasters – the Indian Ocean

tsunami and the South Asia earthquake. The tsunami killed over

10,000 people in India, and the earthquake over 2,000.

Each year, India suffers disaster losses of USD1 billion accord-

ing to World Bank studies.

3

On average, direct natural disaster

losses amount to two per cent of India’s gross domestic product

and up to 12 per cent of central government revenues.

4

These

estimates do not fully include losses incurred by informal sector

businesses and workers, which constitute a major proportion of

India’s economy. The Calamity Relief Fund of the Government

of India spends USD286 million towards providing relief to the

victims of disasters. Over the past 35 years, India has suffered

direct losses of USD30 billion. Losses are also increasing: USD9

billion of direct losses were suffered between 1996 and 2000

alone.

5

The 2001 Gujarat earthquake caused losses of USD2.7

billion.

6

The price tags of the tsunami and South Asia earthquake

are surely enormous but are yet to be seen.

Assuming that the impact of natural disasters remains at this level

(and many estimates predict an increase), how will India cope, let

alone use the benefits of economic development to uplift the

millions of poor? Poor countries are the most adversely affected by

natural hazards, and the poor within those countries face the great-

est difficulties. Their small but important assets are often unsecured,

and their financial risks are not spread across insurance markets.

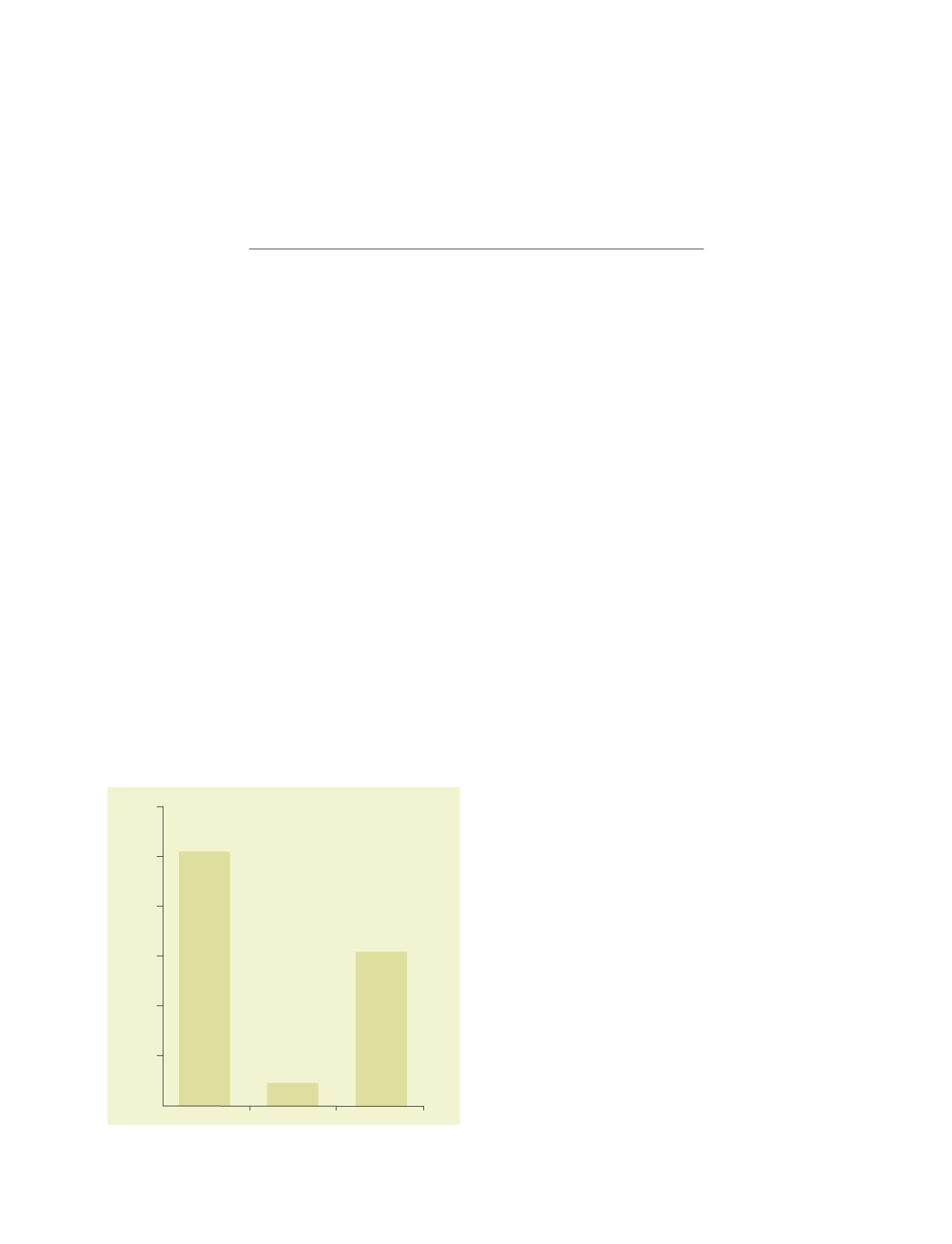

According to the Munich Re Group’s Annual Review:

Natural

Catastrophes 2005

, the proportion of disaster losses in 2005 covered

by insurance were 51 per cent for the Americas and 30 per cent

for Europe. Over the same period, only five per cent of losses in

Asian countries were covered by insurance. Even within Asia, it is

mostly the wealthy that purchase and use insurance.

It has been the experience of AIDMI that the poor, especially

the poor amongst disaster victims, are repeatedly exposed to and

affected by disaster. Their access to vital financial services is also

perpetually restricted. This increases vulnerability to future disas-

ter-induced loss, and impedes sustainable recovery and long-term

development. AIDMI has found that for the most vulnerable

sectors of society, there is a substantial lack of viable options for

reducing and transferring risk. This is true before disasters, but

particularly acute during relief provision.

Taking risk off the backs of the poor:

Afat Vimo

disaster insurance

Mihir R. Bhatt with Mehul Pandya and Tommy Reynolds

All India Disaster Mitigation Institute

America

10

0

20

30

40

50

60

Asia

Europe

Percentage covered

Percentage of 2005 disaster losses covered by insurance

Source: Munich Re (2006). Topics Geo. Annual Review: Natural Catastrophes 2005